Complete Guide to Negotiate Insurance Contract Rates for Medical Practices

According to the Medical Group Management Association (MGMA), about 58 percent of medical group leaders review payer contracts annually. While more than half is great, the number of practices that then proceed to contact payers and initiate negotiations is far fewer. If your practice falls into that category, you're leaving money on the table.

The truth is that most providers aren't reaching their full revenue potential, and it's a costly mistake that many can't afford to keep making. Administrative costs are at an all-time high, with some estimates showing that the U.S. spends a whopping $1.1 trillion annually on these tasks alone. Practices spend considerable resources, yet lose up to 11 percent of their net annual revenue due to insurance underpayments and even more from unfair contract rates.

All these issues compound, placing significant financial strain on practices nationwide. About 90 percent of medical practices reported higher operating costs in 2025 compared to 2024, with expenses quickly outpacing revenue growth. The Healthcare Financial Management Association (HFMA) estimates that hospitals and health systems need to negotiate a 5 to 8 percent increase each year to break even by 2027.

Strategic contract negotiations can make a significant difference for medical practices like yours. With the right approach, you can negotiate better insurance contract terms, boosting your practice's revenue by 15 to 25 percent, all without adding new patients. In this guide, we'll explore several proven strategies that can help you secure higher insurance reimbursement rates that will maximize revenue and put your practice on the path toward financial success and stability.

Essential Steps for Successful Insurance Contract Negotiation

Negotiating higher insurance payments can be overwhelming, and it's not a quick process. Payers typically hold the upper hand due to their significant market power and financial leverage, especially when compared to individual practices or smaller group practices. However, that doesn't mean payer contract optimization isn't possible. There are many ways to negotiate better terms that benefit your practice and its bottom line.

Before initiating negotiations, it is essential to understand the process, conduct thorough due diligence and develop a strategy that positions your practice for success. Here's what a typical negotiation process entails for medical practices.

• Identify Negotiation Targets: The first thing to do is identify your negotiation target. Audit current contracts and analyze your practice's payer mix. Depending on your practice's specialty, you may have well over 25 different payer contracts. To optimize this process, you must determine which insurers cover the most significant percentage of your patient base. Payer contract optimization is all about focusing your efforts on the insurers that contribute the most to your annual revenue. Use your audit findings to identify which payers account for the majority of your revenue and those that pay below market rates.

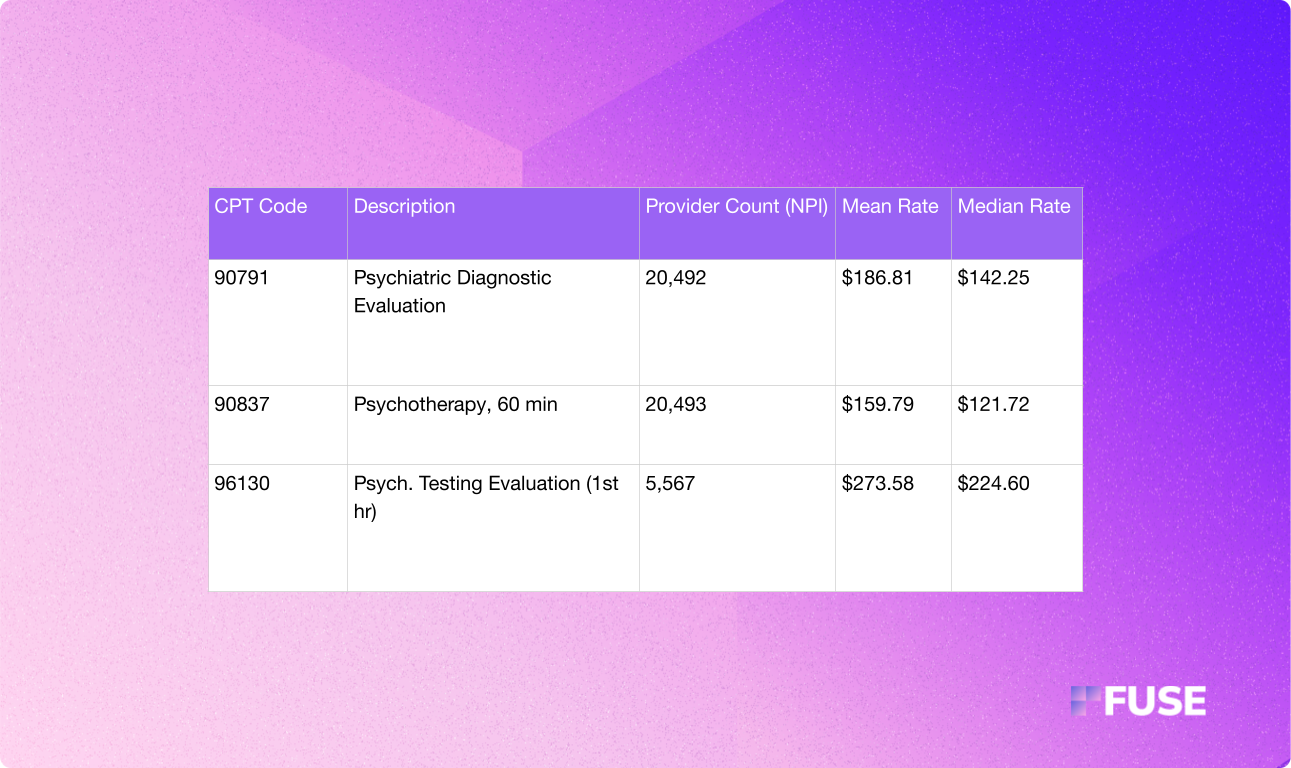

• Identify Revenue Drivers: Next, you must identify where most of your practice's revenue comes from. You don't want to waste energy, resources or leverage to get better insurance reimbursement rates across the board. Instead, set your sights on the CPT codes that move the needle most for your practice. Follow the 80/20 rule. Typically, about 80 percent of a practice's revenue comes from just 20 percent of CPT codes used to bill payers. Use that rule to understand what rates should be up for negotiations.

• Data Collection: Don't expect to get better insurance contract terms without supplying concrete data. Before proceeding with any negotiations, you must collect data about current reimbursement rates, payment deadlines, increase clauses and more. Understand your current contract. Then, collect data about your practice. Know your numbers and prepare to present information about current overhead and operating costs. This information can help you build a case when negotiating with payers.

• Conduct Market Rate Analysis: Of course, you can't build a case if you don't understand how your current insurance contract terms compare to what's normal for the market. Know where your current reimbursement rates stand in relation to market norms. There are many ways to competitively position your practice, but proving that your rates are below market goes a long way. Perform comprehensive market rate analysis. Many resources are available. Take advantage of price transparency data, now available as part of a CMS mandate, MGMA data, information from state medical organizations and more to learn where your rates currently stand.

• Build a Value Proposition: The most significant challenge when negotiating medical provider contracts with payers is building a case as to why your practice deserves better. The information you uncover during market rate analysis makes a difference. However, you also need to develop a value proposition. Use data to show how your practice provides value to a payer's members. We'll get into the specifics of building your case soon, but it's essential to understand that this step in the process focuses solely on what your practice has to offer patients. It's about showing payers why your practice deserves more favorable insurance reimbursement rates.

• Initiate Negotiations: Once you complete your due diligence and preparations, you can initiate negotiations. However, there are timing considerations. Review the current contract terms and renewal dates to determine the best time to start negotiations. Learn about any increase clauses or auto-renewal dates. Negotiations take time, and it's typically best to start negotiating better terms roughly three to six months before contract renewal, if not sooner.

• Back-and-Forth Discussions: Negotiations are rarely one-and-done. Expect a back-and-forth with payers. Set realistic targets and consider broadening the scope of your negotiations. In addition to fighting to increase reimbursement rates, you can negotiate other terms. For example, discussing faster payment cycles, improved claims appeal processes and other specifics within payer contracts can lead to better outcomes for your practice.

• Execution and Follow-Through: After signing new insurance contract terms, monitor reimbursements and look out for underpayments to ensure payers are holding up their end of your new agreement.

Payer Contract Optimization: Building Your Foundation

Building a strong case before you negotiate insurance contract rates can make all the difference. While healthcare providers spend their days helping patients, insurance is ultimately all about business. Payers will fight to keep rates low, so it's up to practices to take the initiative, do their homework and create a rock-solid argument as to why payer contracts need review and change.

To achieve this, you must start with a solid foundation. Payer contracts are legally binding agreements that outline how a health insurance company will reimburse a healthcare provider for services provided to its policyholders. It sounds simple enough, but there are many different types of payer contracts and countless terms to understand.

Before negotiations, take the time to audit your current contracts. You want to review all terms and fee schedules. More importantly, you must collect data about your practice and market standards to understand how your current contract affects your business.

Comparing Fee Schedules and Actual Payments

When reviewing contracts with each payer your practice works with, analyze the agreed-upon fee schedules and actual payments made to your practice. Fee schedules reflect insurance reimbursement rates for specific CPT codes. Most practices follow a traditional fee-for-service (FFS) model where insurance companies pay a set fee each time a practice provides a particular service. However, that doesn't mean your practice always receives the amount covered in the fee schedule.

Actual remittances after claims processing are often lower. As mentioned earlier, underpayment is common, and practices can lose up to 11 percent of annual revenue to insurance underpayment if not caught. Underpayment can occur for many reasons, including downcoding, processing errors or unfavorable bundle rules. Whatever the case, you want to understand how underpayment affects your practice and use that information to build your case.

When auditing your contract, pull the top CPT codes and compare the contracted fee schedule to payments received by the payer. You'll likely find discrepancies. Flag them and collect all relevant data to prove your case during negotiations.

Identifying Weak Clauses

Insurance contract terms can significantly impact revenue in various ways. It's not just about fee schedules and CPT codes. Weak or risky clauses in your contract could also hurt your practice. Successful payer contract optimization involves identifying and addressing key clauses during the negotiation process.

There are many red flags to look for when reviewing contracts. Some of the biggest include:

• Strict Prior Authorization Requirements: Excessive limitations and rules about prior authorizations can severely limit revenue. Furthermore, it can disrupt and delay patient care, ultimately impacting a practice's ability to provide high-quality service.

• Unilateral Amendment Clauses: Some contracts have clauses that allow insurance companies to change terms without consulting a practice, which can be a nightmare for providers.

• Auto-Renewal Clauses: Many contracts have auto-renewal clauses, which can lock practices into outdated rates.

• Termination Clauses: If a contract has clauses that allow insurers to drop practices without cause, practices will have less leverage during negotiations.

•Unclear Payment Timelines: Contracts should have clear timelines that dictate how quickly payers process and remit payments to practices. If they don't, practices will have unpredictable revenue.

• No Escalation Terms: Some payer contracts lack escalation terms that increase rates annually. Thus, rates can quickly fall behind inflation and rising operating costs.

Understanding Non-Rate Insurance Contract Terms

Additional insurance contract terms can negatively impact revenue, resulting in underpayments, increased losses and unnecessary complexity. Familiarize yourself with existing downcoding policies, bundling rules and dispute resolution processes. Collect data to understand how these terms affect your practice's revenue, and flag issues that you can use to create leverage during negotiations.

Benchmarking

After you audit your current insurance contract terms, you must perform market rate analysis to benchmark your insurance reimbursement rates against Medicare and market standards.

Medicare is a universal benchmark. Reimbursement rates follow federal law. Therefore, the annually published Physician Fee Schedule serves as a valuable reference point for comparing payer reimbursement rates. Many commercial insurance companies express rates as a percentage of Medicare. For example, your contract may express a rate for a specific CPT code as 110 percent of Medicare, meaning the payer reimburses 110 percent of what Medicare would pay.

Compare your contract rates to current Medicare rates. Any rate below 100 percent of Medicare indicates that it's below industry norms.

Don't stop with Medicare benchmarking. It's also important to compare your practice's rates with local and national benchmarks. CMS now requires all payers to publish all negotiated rates each month into Machine Readable Files. Several firms, including Fuse, offer services to help analyze this data to benchmark your rates against competitors.

Proven Strategies for Higher Insurance Payments

Payer contract optimization can be daunting. However, if you take the time to prepare and collect data, you can easily develop a strategy that works in your practice's favor. There are many tactics you can employ. Let's explore some of the most effective.

Get Higher Insurance Payments By Leveraging Patient Volume

Volume-based rate increases are another strategy that practices can leverage to great success. Payers are more likely to increase reimbursement rates if a practice can demonstrate that it serves a significant number of in-network patients. Insurance companies don't want to lose patients if a practice decides to leave a network. Therefore, considerable volume is a powerful bargaining chip.

Here's where data collection and analysis make a difference. During your negotiations, prove that your practice can drive referrals and reduce out-of-network leakage. Demonstrate that your practice is a go-to for a payer's members in your area, and highlight how leaving the network could impact the payer's bottom line. Utilize billing reports and EMR data to demonstrate the value of your practice.

That data can be the tipping point for insurance companies. You may even have enough leverage to propose a tiered rate increase. Tie insurance reimbursement rate increases to patient volume benchmarks. This approach reframes negotiations, turning your request for increased rates into a mutually beneficial arrangement.

Propose Multi-Year Agreements with Incremental Increases

Rather than asking for immediate improvements to your medical provider contracts, you can propose multi-year agreements with smaller annual rate increases. This strategy is often more successful than sudden rate increases, as it allows payers to adjust terms over time while securing your in-network partnership for a longer period.

Consider proposing a multi-year agreement with a clause that covers predetermined rate escalators. For example, you can agree to a five-year contract with annual rate increases of 2 to 4 percent. This type of agreement will protect your practice from inflation and increasing operating costs. More importantly, it prevents rate stagnation while providing more predictable revenue.

When developing your proposal, use patient volume data to demonstrate that your practice will continue to be a valuable asset to the payer's network.

Highlighting the Value Your Practice Provides to Create a Win-Win Scenario for Payers

Does your practice offer something that others can't? If so, use it to negotiate insurance contract rates that increase your revenue potential. Think about what sets your practice apart from the competition.

One of the most common bargaining chips is scarcity. For example, your practice might offer family care in a Medically Underserved Area. If your practice serves a remote location without many providers for patients to turn to, you have more bargaining power than you might realize.

Another common scenario is that you offer a specialty that few others in the geographic region do. Patients often prefer not to drive hours to see a specialist. If you're the only neurosurgeon in town, payers are more likely to increase reimbursement rates to keep you in-network.

Approaching Insurance Companies: Preparation Phase

We've already covered the importance of collecting and analyzing data. However, you must strategically present that information to ensure that you have all the necessary bargaining power to achieve success.

Before approaching insurance companies, gather data on practice performance, patient volume and other relevant metrics. Payers want to see value. When you can show that your practice provides value to the insurance network, you're more likely to get better insurance reimbursement rates.

Volume is always important. However, our data should also reflect clinical outcomes and the overall patient experience. Participate in CMS programs, score high on CAHPS surveys and collect data that shows positive patient outcomes. Lower hospital readmission rates, reduced infection rates, a higher volume of screenings, more frequent preventative care and other critical metrics can showcase that your practice is making a difference. You can even showcase great patient reviews your practice receives online.

Your goal is to show that your practice provides value that aligns with a payer's priorities. A payer's priorities are to deliver value-based care while improving patient outcomes. If you can prove that your practice does that, you have a strong case for better insurance contract terms.

It's also vital that you perform competitor analysis. Show how your rates, performance and patient outcomes compare to competitor practices, especially those that are within a payer's network.

The Centers for Medicare & Medicaid Services (CMS) requires that all payers publish their negotiated rates. That data lives in massive datasets called Machine-Readable Files (MRFs). Companies like Fuse can extract, interpret and benchmark negotiated rates, providing actionable insights and information that practices can use during rate negotiations.

Study that data to build your case and include it in a clear and concise proposal packet. These packets should provide strong evidence of value that justifies your insurance reimbursement rate increase.

Maximizing Insurance Reimbursement Rates Through Strategic Timing

Proper timing can make or break your success when you negotiate insurance contract rates. When determining the optimal time to initiate negotiations, consider budget planning periods and renewal cycles.

Most insurance companies finalize annual budgets in late Q3 or early Q4. It's best to propose new insurance contract terms when payers finalize their budgets. If you do so afterward, there will be less flexibility from payers. Therefore, you have less leverage.

Contracts typically last one to three years. The best time to renegotiate terms is approximately three to six months before renewal. Any sooner, and you won't have much bargaining power. However, if you wait too long, you risk a tight negotiation schedule that may not reach its conclusion before your contract automatically renews at inferior rates.

The best approach is to develop and maintain a renewal schedule. Prepare early and create data-rich proposal packages you can submit at the right time.

Finally, consider how often you request negotiations. If you recently received an increase in insurance reimbursement rates in the last year, it's more challenging to get payers to engage in discussions. You don't want to request increases too often.

Remain Human

Our last tip is an easy one: Be kind and remain professional when negotiating with payer reps. It always pays to develop a rapport with the representatives you interact with. Build a strong professional relationship from the start, and representatives are more likely to engage with you when it's time to renegotiate insurance contract terms.

It's always good to remain firm. You want to do what's best for your practice. However, never approach negotiations from a place of hostility. That rarely works in a practice's favor, often backfiring. Instead, be cordial and present your case with data. Data-backed proposals pack a more potent punch than any form of aggression. Show payers precisely why your practice deserves better rates, backing everything you propose with concise data.

Transform Your Practice Revenue with Expert Contract Support

Negotiating an increase in reimbursement rates can be a challenging process that requires significant preparation and thorough data analysis. However, your practice doesn't have to approach negotiations alone. Expert analysis and support can give you a competitive edge, ensuring you have as much bargaining power as possible.

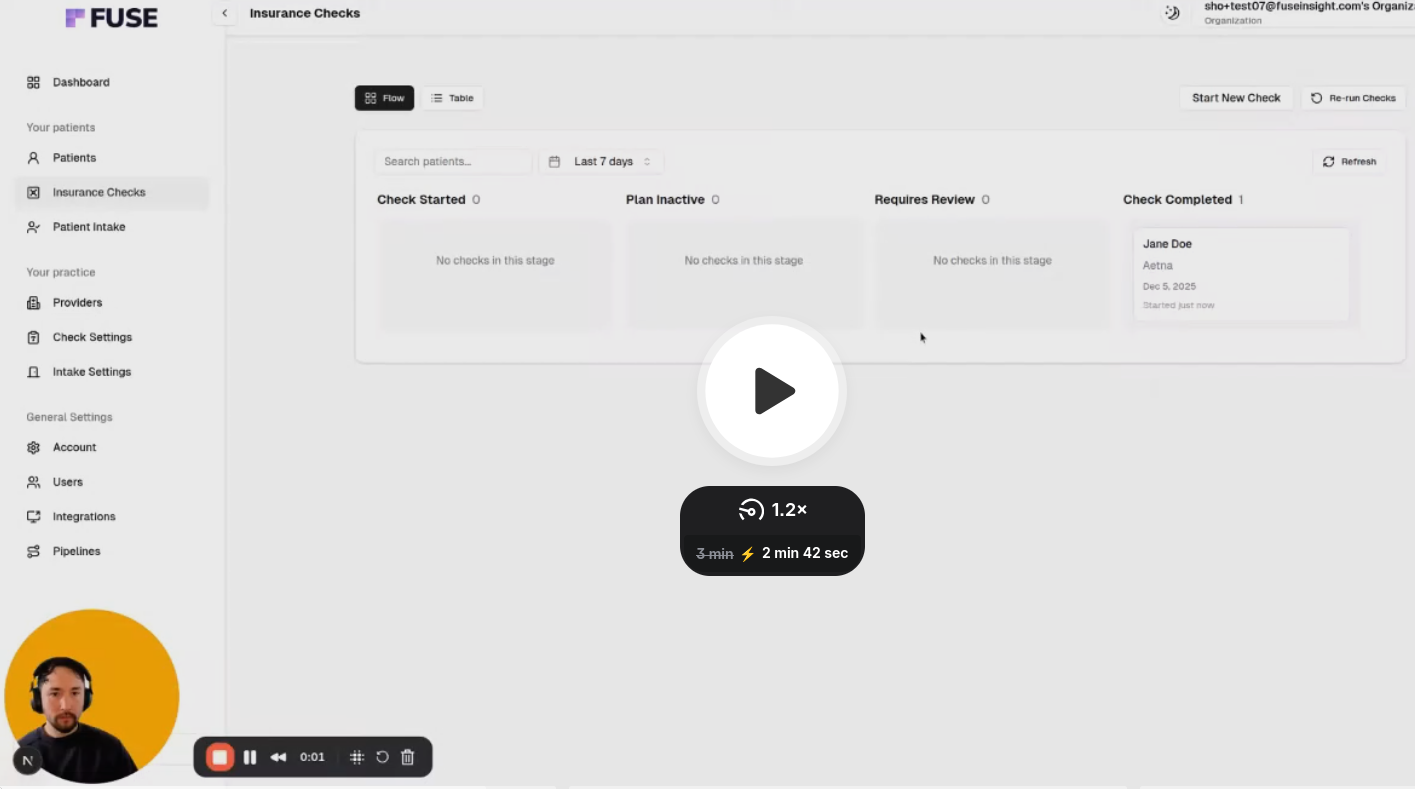

Fuse can provide expert guidance when navigating complex payer relationships. Fuse can automate patient intake and perform CPT code-level insurance verification. With Fuse, practices like yours can significantly reduce administrative friction while potentially achieving a return on your professional assistance investment. When it comes time for your practice to negotiate insurance contract rates, Fuse can analyze, interpret and benchmark data within MRFs, providing you with all the information you need to negotiate better contract terms with confidence. Not only can Fuse support negotiations with data, but it can also offer additional services, such as intake, verification, and more.

Schedule your demo with Fuse today to learn more about how it can transform your practice and empower you with the data needed to negotiate insurance contract rates that lead to more revenue.

According to the Medical Group Management Association (MGMA), about 58 percent of medical group leaders review payer contracts annually. While more than half is great, the number of practices that then proceed to contact payers and initiate negotiations is far fewer. If your practice falls into that category, you're leaving money on the table.

The truth is that most providers aren't reaching their full revenue potential, and it's a costly mistake that many can't afford to keep making. Administrative costs are at an all-time high, with some estimates showing that the U.S. spends a whopping $1.1 trillion annually on these tasks alone. Practices spend considerable resources, yet lose up to 11 percent of their net annual revenue due to insurance underpayments and even more from unfair contract rates.

All these issues compound, placing significant financial strain on practices nationwide. About 90 percent of medical practices reported higher operating costs in 2025 compared to 2024, with expenses quickly outpacing revenue growth. The Healthcare Financial Management Association (HFMA) estimates that hospitals and health systems need to negotiate a 5 to 8 percent increase each year to break even by 2027.

Strategic contract negotiations can make a significant difference for medical practices like yours. With the right approach, you can negotiate better insurance contract terms, boosting your practice's revenue by 15 to 25 percent, all without adding new patients. In this guide, we'll explore several proven strategies that can help you secure higher insurance reimbursement rates that will maximize revenue and put your practice on the path toward financial success and stability.

Essential Steps for Successful Insurance Contract Negotiation

Negotiating higher insurance payments can be overwhelming, and it's not a quick process. Payers typically hold the upper hand due to their significant market power and financial leverage, especially when compared to individual practices or smaller group practices. However, that doesn't mean payer contract optimization isn't possible. There are many ways to negotiate better terms that benefit your practice and its bottom line.

Before initiating negotiations, it is essential to understand the process, conduct thorough due diligence and develop a strategy that positions your practice for success. Here's what a typical negotiation process entails for medical practices.

• Identify Negotiation Targets: The first thing to do is identify your negotiation target. Audit current contracts and analyze your practice's payer mix. Depending on your practice's specialty, you may have well over 25 different payer contracts. To optimize this process, you must determine which insurers cover the most significant percentage of your patient base. Payer contract optimization is all about focusing your efforts on the insurers that contribute the most to your annual revenue. Use your audit findings to identify which payers account for the majority of your revenue and those that pay below market rates.

• Identify Revenue Drivers: Next, you must identify where most of your practice's revenue comes from. You don't want to waste energy, resources or leverage to get better insurance reimbursement rates across the board. Instead, set your sights on the CPT codes that move the needle most for your practice. Follow the 80/20 rule. Typically, about 80 percent of a practice's revenue comes from just 20 percent of CPT codes used to bill payers. Use that rule to understand what rates should be up for negotiations.

• Data Collection: Don't expect to get better insurance contract terms without supplying concrete data. Before proceeding with any negotiations, you must collect data about current reimbursement rates, payment deadlines, increase clauses and more. Understand your current contract. Then, collect data about your practice. Know your numbers and prepare to present information about current overhead and operating costs. This information can help you build a case when negotiating with payers.

• Conduct Market Rate Analysis: Of course, you can't build a case if you don't understand how your current insurance contract terms compare to what's normal for the market. Know where your current reimbursement rates stand in relation to market norms. There are many ways to competitively position your practice, but proving that your rates are below market goes a long way. Perform comprehensive market rate analysis. Many resources are available. Take advantage of price transparency data, now available as part of a CMS mandate, MGMA data, information from state medical organizations and more to learn where your rates currently stand.

• Build a Value Proposition: The most significant challenge when negotiating medical provider contracts with payers is building a case as to why your practice deserves better. The information you uncover during market rate analysis makes a difference. However, you also need to develop a value proposition. Use data to show how your practice provides value to a payer's members. We'll get into the specifics of building your case soon, but it's essential to understand that this step in the process focuses solely on what your practice has to offer patients. It's about showing payers why your practice deserves more favorable insurance reimbursement rates.

• Initiate Negotiations: Once you complete your due diligence and preparations, you can initiate negotiations. However, there are timing considerations. Review the current contract terms and renewal dates to determine the best time to start negotiations. Learn about any increase clauses or auto-renewal dates. Negotiations take time, and it's typically best to start negotiating better terms roughly three to six months before contract renewal, if not sooner.

• Back-and-Forth Discussions: Negotiations are rarely one-and-done. Expect a back-and-forth with payers. Set realistic targets and consider broadening the scope of your negotiations. In addition to fighting to increase reimbursement rates, you can negotiate other terms. For example, discussing faster payment cycles, improved claims appeal processes and other specifics within payer contracts can lead to better outcomes for your practice.

• Execution and Follow-Through: After signing new insurance contract terms, monitor reimbursements and look out for underpayments to ensure payers are holding up their end of your new agreement.

Payer Contract Optimization: Building Your Foundation

Building a strong case before you negotiate insurance contract rates can make all the difference. While healthcare providers spend their days helping patients, insurance is ultimately all about business. Payers will fight to keep rates low, so it's up to practices to take the initiative, do their homework and create a rock-solid argument as to why payer contracts need review and change.

To achieve this, you must start with a solid foundation. Payer contracts are legally binding agreements that outline how a health insurance company will reimburse a healthcare provider for services provided to its policyholders. It sounds simple enough, but there are many different types of payer contracts and countless terms to understand.

Before negotiations, take the time to audit your current contracts. You want to review all terms and fee schedules. More importantly, you must collect data about your practice and market standards to understand how your current contract affects your business.

Comparing Fee Schedules and Actual Payments

When reviewing contracts with each payer your practice works with, analyze the agreed-upon fee schedules and actual payments made to your practice. Fee schedules reflect insurance reimbursement rates for specific CPT codes. Most practices follow a traditional fee-for-service (FFS) model where insurance companies pay a set fee each time a practice provides a particular service. However, that doesn't mean your practice always receives the amount covered in the fee schedule.

Actual remittances after claims processing are often lower. As mentioned earlier, underpayment is common, and practices can lose up to 11 percent of annual revenue to insurance underpayment if not caught. Underpayment can occur for many reasons, including downcoding, processing errors or unfavorable bundle rules. Whatever the case, you want to understand how underpayment affects your practice and use that information to build your case.

When auditing your contract, pull the top CPT codes and compare the contracted fee schedule to payments received by the payer. You'll likely find discrepancies. Flag them and collect all relevant data to prove your case during negotiations.

Identifying Weak Clauses

Insurance contract terms can significantly impact revenue in various ways. It's not just about fee schedules and CPT codes. Weak or risky clauses in your contract could also hurt your practice. Successful payer contract optimization involves identifying and addressing key clauses during the negotiation process.

There are many red flags to look for when reviewing contracts. Some of the biggest include:

• Strict Prior Authorization Requirements: Excessive limitations and rules about prior authorizations can severely limit revenue. Furthermore, it can disrupt and delay patient care, ultimately impacting a practice's ability to provide high-quality service.

• Unilateral Amendment Clauses: Some contracts have clauses that allow insurance companies to change terms without consulting a practice, which can be a nightmare for providers.

• Auto-Renewal Clauses: Many contracts have auto-renewal clauses, which can lock practices into outdated rates.

• Termination Clauses: If a contract has clauses that allow insurers to drop practices without cause, practices will have less leverage during negotiations.

•Unclear Payment Timelines: Contracts should have clear timelines that dictate how quickly payers process and remit payments to practices. If they don't, practices will have unpredictable revenue.

• No Escalation Terms: Some payer contracts lack escalation terms that increase rates annually. Thus, rates can quickly fall behind inflation and rising operating costs.

Understanding Non-Rate Insurance Contract Terms

Additional insurance contract terms can negatively impact revenue, resulting in underpayments, increased losses and unnecessary complexity. Familiarize yourself with existing downcoding policies, bundling rules and dispute resolution processes. Collect data to understand how these terms affect your practice's revenue, and flag issues that you can use to create leverage during negotiations.

Benchmarking

After you audit your current insurance contract terms, you must perform market rate analysis to benchmark your insurance reimbursement rates against Medicare and market standards.

Medicare is a universal benchmark. Reimbursement rates follow federal law. Therefore, the annually published Physician Fee Schedule serves as a valuable reference point for comparing payer reimbursement rates. Many commercial insurance companies express rates as a percentage of Medicare. For example, your contract may express a rate for a specific CPT code as 110 percent of Medicare, meaning the payer reimburses 110 percent of what Medicare would pay.

Compare your contract rates to current Medicare rates. Any rate below 100 percent of Medicare indicates that it's below industry norms.

Don't stop with Medicare benchmarking. It's also important to compare your practice's rates with local and national benchmarks. CMS now requires all payers to publish all negotiated rates each month into Machine Readable Files. Several firms, including Fuse, offer services to help analyze this data to benchmark your rates against competitors.

Proven Strategies for Higher Insurance Payments

Payer contract optimization can be daunting. However, if you take the time to prepare and collect data, you can easily develop a strategy that works in your practice's favor. There are many tactics you can employ. Let's explore some of the most effective.

Get Higher Insurance Payments By Leveraging Patient Volume

Volume-based rate increases are another strategy that practices can leverage to great success. Payers are more likely to increase reimbursement rates if a practice can demonstrate that it serves a significant number of in-network patients. Insurance companies don't want to lose patients if a practice decides to leave a network. Therefore, considerable volume is a powerful bargaining chip.

Here's where data collection and analysis make a difference. During your negotiations, prove that your practice can drive referrals and reduce out-of-network leakage. Demonstrate that your practice is a go-to for a payer's members in your area, and highlight how leaving the network could impact the payer's bottom line. Utilize billing reports and EMR data to demonstrate the value of your practice.

That data can be the tipping point for insurance companies. You may even have enough leverage to propose a tiered rate increase. Tie insurance reimbursement rate increases to patient volume benchmarks. This approach reframes negotiations, turning your request for increased rates into a mutually beneficial arrangement.

Propose Multi-Year Agreements with Incremental Increases

Rather than asking for immediate improvements to your medical provider contracts, you can propose multi-year agreements with smaller annual rate increases. This strategy is often more successful than sudden rate increases, as it allows payers to adjust terms over time while securing your in-network partnership for a longer period.

Consider proposing a multi-year agreement with a clause that covers predetermined rate escalators. For example, you can agree to a five-year contract with annual rate increases of 2 to 4 percent. This type of agreement will protect your practice from inflation and increasing operating costs. More importantly, it prevents rate stagnation while providing more predictable revenue.

When developing your proposal, use patient volume data to demonstrate that your practice will continue to be a valuable asset to the payer's network.

Highlighting the Value Your Practice Provides to Create a Win-Win Scenario for Payers

Does your practice offer something that others can't? If so, use it to negotiate insurance contract rates that increase your revenue potential. Think about what sets your practice apart from the competition.

One of the most common bargaining chips is scarcity. For example, your practice might offer family care in a Medically Underserved Area. If your practice serves a remote location without many providers for patients to turn to, you have more bargaining power than you might realize.

Another common scenario is that you offer a specialty that few others in the geographic region do. Patients often prefer not to drive hours to see a specialist. If you're the only neurosurgeon in town, payers are more likely to increase reimbursement rates to keep you in-network.

Approaching Insurance Companies: Preparation Phase

We've already covered the importance of collecting and analyzing data. However, you must strategically present that information to ensure that you have all the necessary bargaining power to achieve success.

Before approaching insurance companies, gather data on practice performance, patient volume and other relevant metrics. Payers want to see value. When you can show that your practice provides value to the insurance network, you're more likely to get better insurance reimbursement rates.

Volume is always important. However, our data should also reflect clinical outcomes and the overall patient experience. Participate in CMS programs, score high on CAHPS surveys and collect data that shows positive patient outcomes. Lower hospital readmission rates, reduced infection rates, a higher volume of screenings, more frequent preventative care and other critical metrics can showcase that your practice is making a difference. You can even showcase great patient reviews your practice receives online.

Your goal is to show that your practice provides value that aligns with a payer's priorities. A payer's priorities are to deliver value-based care while improving patient outcomes. If you can prove that your practice does that, you have a strong case for better insurance contract terms.

It's also vital that you perform competitor analysis. Show how your rates, performance and patient outcomes compare to competitor practices, especially those that are within a payer's network.

The Centers for Medicare & Medicaid Services (CMS) requires that all payers publish their negotiated rates. That data lives in massive datasets called Machine-Readable Files (MRFs). Companies like Fuse can extract, interpret and benchmark negotiated rates, providing actionable insights and information that practices can use during rate negotiations.

Study that data to build your case and include it in a clear and concise proposal packet. These packets should provide strong evidence of value that justifies your insurance reimbursement rate increase.

Maximizing Insurance Reimbursement Rates Through Strategic Timing

Proper timing can make or break your success when you negotiate insurance contract rates. When determining the optimal time to initiate negotiations, consider budget planning periods and renewal cycles.

Most insurance companies finalize annual budgets in late Q3 or early Q4. It's best to propose new insurance contract terms when payers finalize their budgets. If you do so afterward, there will be less flexibility from payers. Therefore, you have less leverage.

Contracts typically last one to three years. The best time to renegotiate terms is approximately three to six months before renewal. Any sooner, and you won't have much bargaining power. However, if you wait too long, you risk a tight negotiation schedule that may not reach its conclusion before your contract automatically renews at inferior rates.

The best approach is to develop and maintain a renewal schedule. Prepare early and create data-rich proposal packages you can submit at the right time.

Finally, consider how often you request negotiations. If you recently received an increase in insurance reimbursement rates in the last year, it's more challenging to get payers to engage in discussions. You don't want to request increases too often.

Remain Human

Our last tip is an easy one: Be kind and remain professional when negotiating with payer reps. It always pays to develop a rapport with the representatives you interact with. Build a strong professional relationship from the start, and representatives are more likely to engage with you when it's time to renegotiate insurance contract terms.

It's always good to remain firm. You want to do what's best for your practice. However, never approach negotiations from a place of hostility. That rarely works in a practice's favor, often backfiring. Instead, be cordial and present your case with data. Data-backed proposals pack a more potent punch than any form of aggression. Show payers precisely why your practice deserves better rates, backing everything you propose with concise data.

Transform Your Practice Revenue with Expert Contract Support

Negotiating an increase in reimbursement rates can be a challenging process that requires significant preparation and thorough data analysis. However, your practice doesn't have to approach negotiations alone. Expert analysis and support can give you a competitive edge, ensuring you have as much bargaining power as possible.

Fuse can provide expert guidance when navigating complex payer relationships. Fuse can automate patient intake and perform CPT code-level insurance verification. With Fuse, practices like yours can significantly reduce administrative friction while potentially achieving a return on your professional assistance investment. When it comes time for your practice to negotiate insurance contract rates, Fuse can analyze, interpret and benchmark data within MRFs, providing you with all the information you need to negotiate better contract terms with confidence. Not only can Fuse support negotiations with data, but it can also offer additional services, such as intake, verification, and more.

Schedule your demo with Fuse today to learn more about how it can transform your practice and empower you with the data needed to negotiate insurance contract rates that lead to more revenue.

FAQs

Most contracts last about one to three years. Trade organizations, such as MGMA, typically recommend reviewing contracts before every renewal to maximize revenue. It's best to negotiate three to six months before the renewal date, with preparation occurring several months earlier.

There is no standard rate increase. It all depends on the current contract terms and the value that practices can prove they provide. Generally, successful negotiations lead to a 5 to 15 percent increase in reimbursement rates.

Market dynamics, network size and the amount of leverage a practice has determine a payer's willingness to negotiate. Typically, mid-sized insurers and regional companies are more likely to negotiate than their larger national counterparts. For smaller insurers, losing a high-volume practice has a bigger impact on network coverage than it does for larger national companies.

Before starting negotiations, you must conduct market rate and competitive analysis. For success, practices must back up negotiations with data. Here's where companies like Fuse come in handy. Fuse can help you interpret data within MRFs, making it easier to see where your practice's rates stand compared to market standards and competitors. It's also important to include metrics covering practice performance, patient volume and patient outcomes in your rate increase proposal packet.

Professional payer contract optimization services are a worthwhile investment. Precise, data-driven cases are key to success, but smaller practices often lack the means to interpret data. MRFs are notorious for being difficult to analyze without advanced data science skills. Contract optimization services can help you utilize MRFs to your advantage, ensuring you have accurate data to support your case during negotiations.

.avif)

.avif)

.avif)

.avif)

.avif)